The Truth About Credit Scores and Buying a Home

Your credit score plays a major role in the homebuying process. It’s one of the key factors lenders look at to determine which loan options you qualify for and the terms you might receive. But there’s a common myth about credit scores that may be holding some buyers back!

The Myth: You Need Perfect Credit

Surprisingly, Fannie Mae reports that only 32% of prospective homebuyers actually understand the credit score requirements set by lenders. That means most people are overestimating what they need!

The Reality: Good Credit Is Often Enough

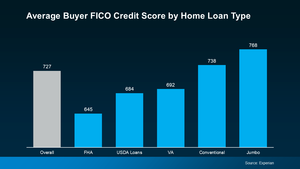

Here’s the truth: You don’t need perfect credit to buy a home. Take a look at the average credit scores of recent homebuyers by loan type (see chart).

Lenders have different levels of risk tolerance and lending strategies. They consider more than just a single “cutoff score.” So even if your score isn’t sky-high, you might still qualify for a mortgage.

That said, while perfect credit isn’t required, a stronger score can open up more loan options and better terms.

Boost Your Score: Simple Steps to Take

Want to expand your options? Here are a few tips from Experian and Freddie Mac:

-

Pay Bills on Time—This includes credit cards, utilities, and every monthly payment. On-time payments build trust with lenders.

-

Lower Your Debt—Paying down balances improves your credit utilization and shows you’re a lower-risk borrower. Better terms may be ahead!

-

Avoid New Credit—Don’t open multiple new accounts quickly. Focus on strengthening the credit you already have.

Bottom Line:

Don’t let the “perfect credit” myth keep you from homeownership. The best first step? Connect with a trusted lender to explore your personal options and gain clarity on where you stand!