Is Your Credit Score Really Holding You Back From Buying a Home?

According to Fannie Mae, 90% of buyers either don’t know the minimum credit score needed for a home loan or overestimate it. That means many people may think homeownership is out of reach—even when it’s not..

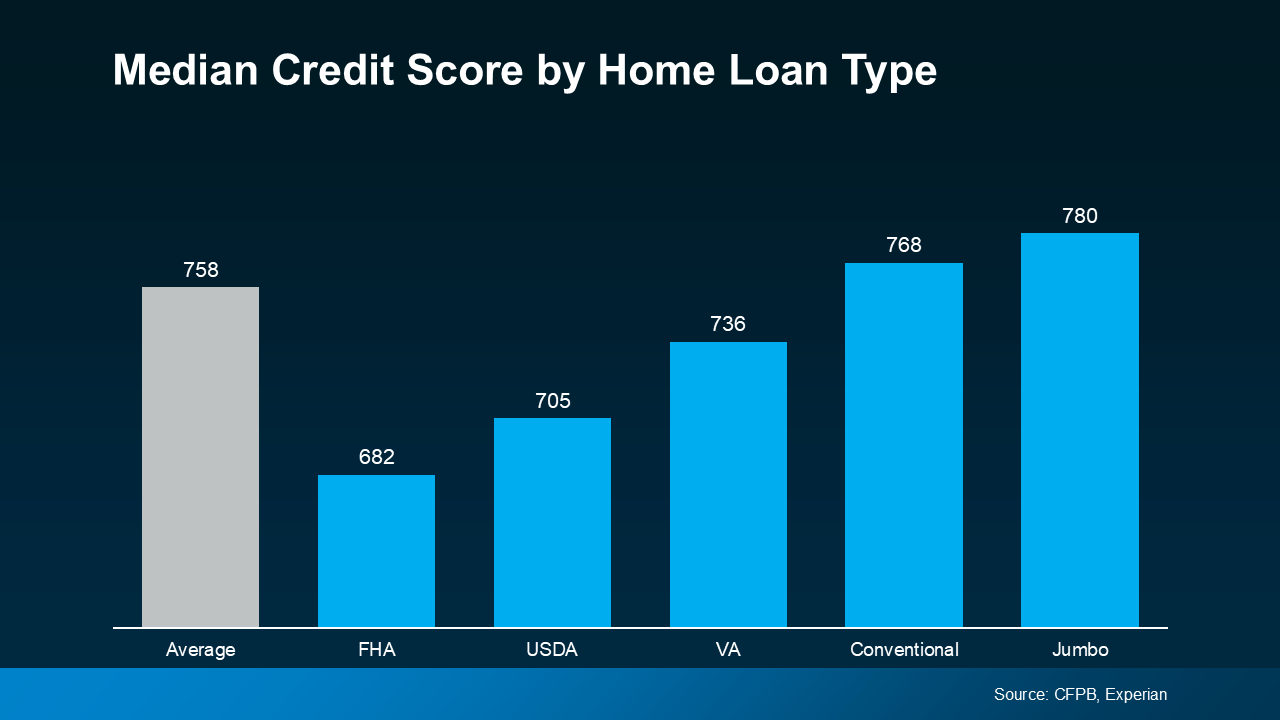

The Truth About Credit Score Requirements

There’s no single credit score required to buy a home. Different loan types have different score averages. This means there’s more flexibility than you might expect. Here’s what you should know:

FHA Loans: While they often allow credit scores as low as 580, the average score for approved FHA loans is currently around 682

VA Loans: May not have a strict minimum score requirement

Conventional Loans: Typically require higher scores, but vary by lender

As FICO explains, there’s no universal cutoff score. Each lender sets its own standards and considers additional factors.

Why Credit Still Matters?

Even though there’s no fixed number, your credit score still plays a key role:

Loan Type Qualification: Certain scores open the door to specific loan programs

Interest Rates: Higher scores usually mean lower mortgage rates

Monthly Payments: Better terms can lead to lower long-term costs

Want To Improve Your Score?

If you want better loan terms, here are a few tips from the Federal Reserve Board:

Pay bills on time to show lenders you’re reliable

Reduce your debt to improve your credit utilization ratio

Review your credit report to fix errors that may be dragging down your score

Avoid opening new accounts before applying for a mortgage

Final Thoughts

Your credit score doesn’t have to be perfect to buy a home. There are options out there, and a trusted lender can help you understand yours. Don’t let misconceptions stop you from starting your journey to homeownership.

This content is for informational purposes only. Always consult with a trusted lender to understand your personal situation and what loan programs might work for you.