Today’s Mortgage Rates Explained

TL;DR

Today’s mortgage rates may feel intimidating, but waiting for the “perfect” rate could cost you more in the long run. As rates approach the psychological 6% mark, more buyers are expected to re-enter the market, increasing competition and pushing prices higher. Acting now can mean more choices, better negotiation power, and long-term savings.

Why Mortgage Rates Feel Scarier Than They Really Are

For many buyers, mortgage rates have become the “monster under the bed.” Every small increase causes hesitation, second thoughts, and the same question: “Should I just wait?”

The truth is, fear around rates is often emotional rather than financial.

Rates today are higher than the historic lows of 2020 and 2021, but those levels were never normal or sustainable. What we’re seeing now is a return to healthier, long-term averages. And while the headlines focus on rate increases, they often ignore the bigger picture—how buyer behavior changes when rates drop even slightly.

The Power of the 6% Mortgage Rate

According to the National Association of Realtors (NAR), a 30-year fixed mortgage rate around 6% is a major psychological tipping point for buyers.

At that level, an estimated 5.5 million more households could afford the median-priced home, including 1.6 million renters. NAR projects that roughly 10% of those households—about 550,000 buyers—would enter the market within 12 to 18 months once rates reach that range.

Why does that matter?

Because when rates approach that “magic number,” buyer confidence rises. Pent-up demand gets unleashed, competition increases, and home prices often follow.

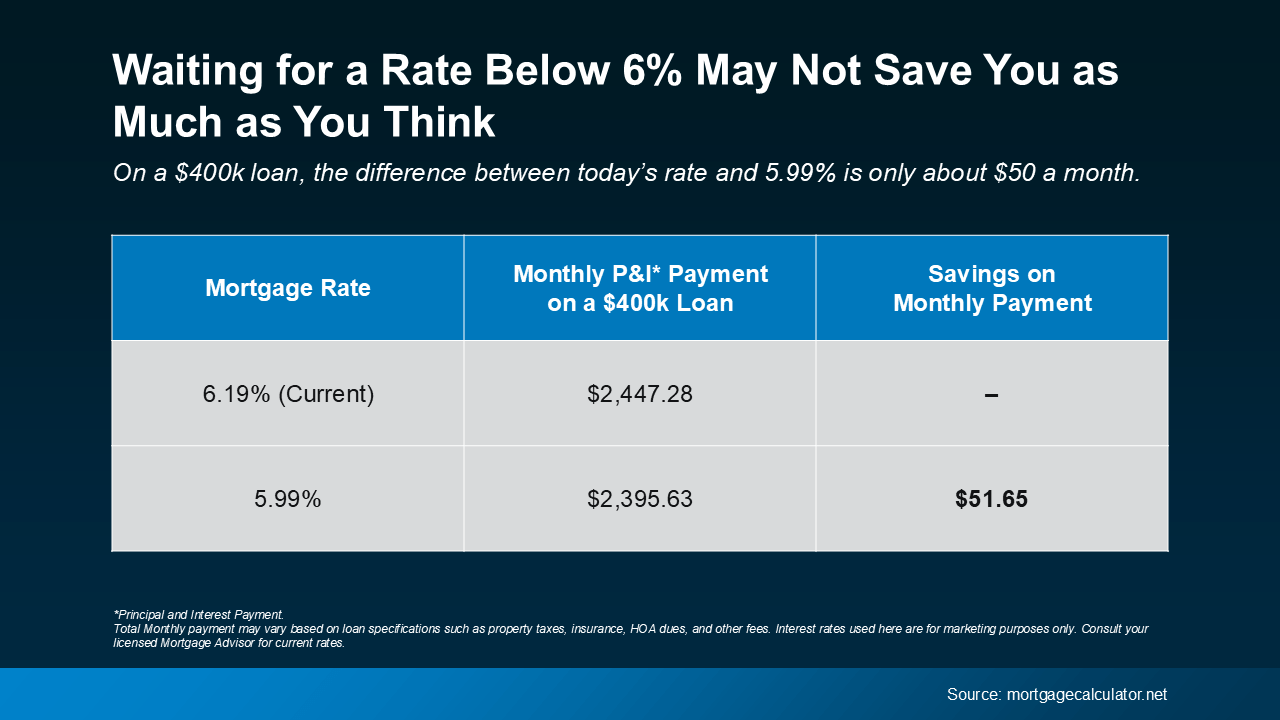

Why Waiting for 5.99% May Not Save You Money

Many buyers believe waiting for a rate under 6% will dramatically lower their monthly payment. In reality, the difference is often much smaller than expected.

On a $400,000 mortgage, the difference between today’s rate (around 6.2%) and 5.99% is roughly $50 per month.

That’s less than what many people spend on coffee, food delivery, or streaming subscriptions. And if home prices rise even modestly once more buyers jump back in, those savings can disappear quickly.

Waiting for a slightly lower rate may actually mean:

Paying more for the home

Competing with more buyers

Losing today’s negotiation leverage

What Buyers Gain by Acting Now

Right now, buyers are in a unique position that may not last long:

More inventory to choose from

Less competition from other buyers

Stronger negotiation power with sellers

More flexibility with inspections, credits, or price adjustments

Once rates dip closer to 6%, many buyers who’ve been sitting on the sidelines are expected to jump back in. When that happens, these advantages often disappear quickly.

Jessica Lautz, Deputy Chief Economist and VP of Research at NAR, explains:

“Over the last several weeks, mortgage rates have averaged just over 6.3%. This has provided savvy buyers a sweet spot to reexamine the home search process with more inventory and wider choices.”

Matt Vernon, Head of Retail Lending at Bank of America, adds:

“Rather than waiting it out for a rate they like better, buyers should assess their personal financial situation. If the home is right and the payments are affordable, it could be the right time to make a move.”

The takeaway? Timing the market perfectly is far less important than buying when the numbers make sense for you.

Bottom Line: Don’t Let Fear Make the Decision

Mortgage rates don’t need to be perfect to make a smart move.

Once rates drop below 6%, competition will likely increase, prices may rise, and buyers could lose the leverage they have today. If you’re financially ready and find the right home, waiting may not pay off the way you expect.

Sometimes, the biggest risk isn’t buying—it’s waiting too long.

Frequently Asked Questions

Q: Are today’s mortgage rates historically high?

A: No. While rates are higher than the pandemic-era lows, they are much closer to long-term historical averages.

Q: Will mortgage rates drop below 6%?

A: Many experts project rates could dip closer to 6% in 2026, but timing and market reactions are unpredictable.

Q: Does a lower rate always mean a better deal?

A: Not necessarily. Lower rates often bring more buyers into the market, which can increase competition and home prices.

Q: Is now a good time for first-time buyers?

A: For many first-time buyers, today’s market offers less competition and more inventory, which can be a big advantage.

Q: How can I know if buying now makes sense for me?

A: Reviewing your finances, goals, and local market conditions is key. Alex Parmenidez can help you evaluate whether now is the right time for your situation.

By Alex Parmenidez, REALTOR® | Coldwell Banker Realty

Alex Parmenidez | Realtor® Licensed CT-MA-RI | Coldwell Banker Realty

196 Waterman St, Providence, RI 02906

C: (401) 426-4825 | O: (401) 351-2017

Check out this article next

Reglas del Depósito de Seguridad en Rhode Island

En Rhode Island, los propietarios pueden cobrar como máximo un mes de renta como depósito de seguridad. Este debe devolverse dentro de los 20 días…

Read Article